A Complete Guide to Sole Trader Tax

November 23, 2021How do I pay tax as a sole trader?

Registering for Self Assessment

What taxes do I need to pay as a sole trader?

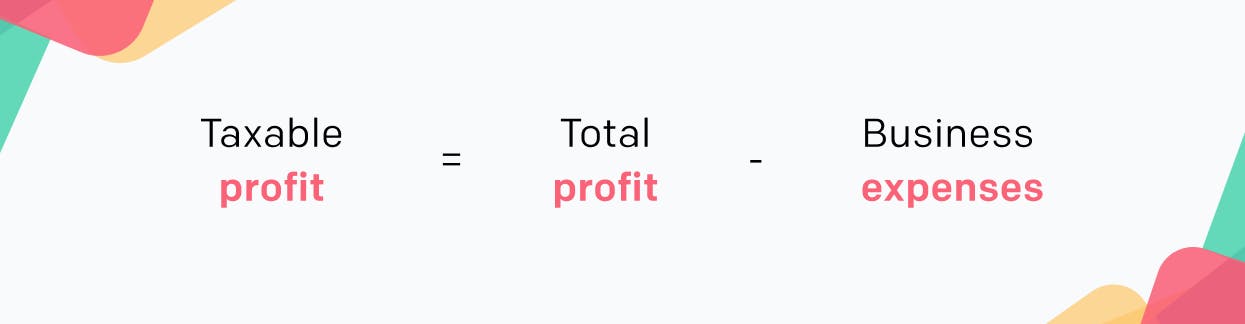

Income Tax

Tax bands

| Band | Personal Allowance | Tax Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 to £50,270 | 20% |

| Higher rate | £50,271 to £150,000 | 40% |

| Additional rate | Over £150,000 | 45% |